Borrowing is an important source of funding for organisations. Understanding how to borrow safely and cost-effectively is a key skill for treasurers. Borrowing green can be cheaper. The potential cost-saving is known as ‘greenium’. But to enjoy greenium savings on our borrowing costs, we must be credibly and consistently green.

Our borrowing cost

One type of borrowing is loans. The main cost of borrowing with loans is interest, together with fees. Another way to borrow is issuing bonds. When we borrow with a bond, we “issue” it.

As the issuer, we create a new transferable instrument – the bond – that evidences our liability to pay interest coupons and repay the principal to the bond holder.

Our cost of borrowing with a bond is known as yield, similar to the interest and fees we pay on a loan. The yield is also the investment rate of return enjoyed by the investors in our bond. Our investors’ income yield is our finance expense as the borrower.

Borrowing with green – or thematic – bonds can be cheaper than with other (“vanilla”) bonds. But any cost savings will depend on the perspectives of our bond investors.

Investors drive our borrowing cost

The yield in the market is determined by the interaction of supply and demand. As issuers, we’d like to sell our bonds into the market – borrowing funds – in a cost-effective manner.

One way to do this is to ensure we are a credibly lower credit risk for investors. A very well-established way of communicating our credit risk is through credit ratings. Credit rating scales are widely understood and generally accepted in the markets. Higher credit-rated bonds – for example, AA – are broadly accepted by investors as being lower risk compared with, for example, B rated bonds.

Ratings focused on green, thematic or ESG (environmental, social and governance) features are not as well-established. Potential related cost savings are known as ‘greenium’ – or green premium.

Premium

In this context, premium means a difference in yields, resulting from attractive – or unattractive - features. For example, credit risk, term and green features. The related premia are known as risk premium, term premium and greenium.

Risk premium

Risk premium refers to the investors’ credit risk, driven in turn by how creditworthy the issuer is. The riskier the investment, the greater the rate of return that investors need. So the costlier it is for us to borrow.

Risk premium is an add-on to yield when credit risk is higher. As the borrower, we would like to reduce the risk premium if we can do it cost-effectively and consistently with our other corporate objectives.

Term premium

Term premium relates to the maturity – or term – of the bond. Investors generally prefer not to tie up their money for too long. So longer maturities – all other things being equal – are less attractive than shorter ones. That being the case, borrowers need to offer higher yields for longer maturities. This element in the total yield is known as term premium.

Like risk premium, term premium is an add-on to yield. The term premium is greater when the term is longer. As the borrower, we need to pay term premium to the investor when we choose to issue longer term bonds.

Greenium

By contrast, greenium is a deduction. When achieved, it reduces yield and our cost of borrowing.

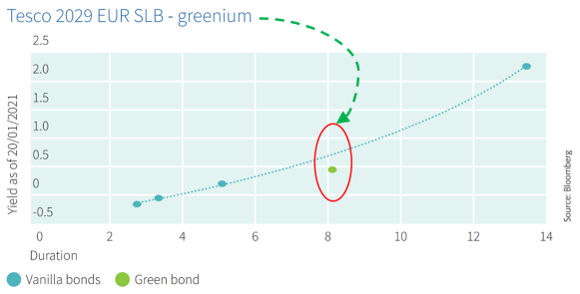

For example, Tesco issued an 8-year Sustainability-Linked Bond (SLB) in 2021. At the same time, it already had a number of ‘vanilla’ bonds – without green features – trading in the market. The yields on these vanilla Tesco bonds are shown on the blue dotted curve below.

The greenium saving for Tesco on the SLB is the vertical distance between the green 8-year bond in the diagram and the dotted blue vanilla yield curve. (Green Bond Pricing in the Primary Market: H1 2022, Climate Bonds Initiative.)

More broadly, greenium is a potential cost-saving for borrowers when they issue any sustainability-themed bonds. Sustainability-themed bonds include green bonds and also other bonds issued by sustainable borrowers, or for sustainable or broader ESG purposes.

Reasons for greenium

There is broad – though not universal – agreement about the existence of the greenium. There is less agreement about the magnitude of the greenium and its likely future trend.

In any event, some investors do seem willing to pay more for green bonds than conventional ones. This results in lower investment yields for the investors, and a reduced cost of borrowing for ourselves when we issue green bonds.

Explanations for some investors’ willingness to pay more for green bonds may include investment funds with mandates to invest in green assets and a shortage of suitable assets in the market.

Borrowing costs and being credibly green

| Green credibility | Investor’s rate of return | Borrower’s cost |

|---|---|---|

| Less credible | Greater | More expensive |

| Highly credible | Lower – acceptable in return for attractiveness of green investment | Cheaper |

As treasurers, it’s very likely our organisation has published an ESG policy. Treasurers need to integrate broader ESG policies within our borrowing strategies. Then be ready to explain to investors.

Greenwashing concerns

"The investor survey reveals a concern about greenwashing. Investors want to be sure that their resources are being allocated to projects that make a difference and have positive impacts."

Green credibility

Potential investors need to be convinced that the statements made by bond issuers are reliable. So as issuers, we need to take steps to ensure our offerings are credible to investors.

External review and greenium

"In terms of bond credibility, we find that only bonds with external review trade at both a statistically and economically significant greenium... We find that only green bonds issued by credible companies trade at a statistically and economically significant greenium."

Summary of our borrowing costs

| Risk premium | Term premium | Greenium | |

|---|---|---|---|

| Feature | How creditworthy we are | Maturity | Thematic labelling |

| Cost of borrowing lowered by | Effective risk management | Shorter term | Credible ESG management |

Cost is not the only consideration for treasurers and their organisations when borrowing. But understanding greenium and its drivers are fundamentally important to borrowing cost-effectively.

___________________

Author: Doug Williamson, FCT

___________________

Are you ready to start learning?

Choose from:

• eLearning courses: 45-90 minutes to complete, available online 24/7.

• training courses: live skills-based training sessions.

• Treasury and Cash Management qualifications: internationally recognised courses from entry to master level. All our courses will provide you with valuable knowledge as well as easy-to-share digital credentials to demonstrate your learning achievements.

More resources

If you found this article helpful, you might also be interested in some of our other resources.