Stakeholders invest their money and other resources in our organisation because they expect us to manage their investment well. If we don’t, stakeholders may withdraw support. So treasurers need to understand stakeholders’ perspectives and how to manage stakeholder value.

Treasury professionals need to understand:

- Who our organisation’s stakeholders are.

- What they do for our organisation.

- What our stakeholders need from us.

- How to manage and balance value for different stakeholders.

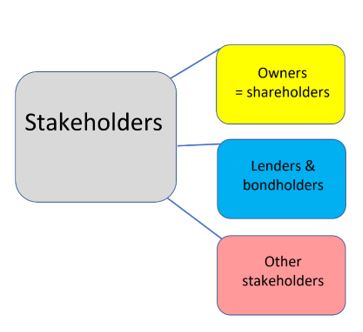

Who are our stakeholders?

Stakeholders are all the individuals, businesses and other entities with a legitimate interest in our organisation’s activities. The stakeholders in our company will always include its shareholders, but also a much wider group of people, organisations and potentially other entities.

For example, one listed health sector business identifies its stakeholders as including customers, employees, suppliers, industry organisations, local and central governments, those who live and work where the business operates, and also society as a whole.

Companies are increasingly - and explicitly - taking account of the interests and capital value of all of these stakeholders, and professional management of the company’s relationships with them, and not just the company’s own shareholders as in the past.

Shareholder value is concerned with the interests of shareholders, primarily their financial interests. Stakeholder value is concerned with the financial and other interests of all stakeholders.

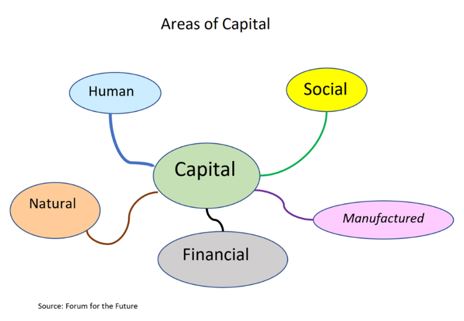

Managing multiple types of capital

Another perspective on the different stakeholders in organisations is to consider the multiple types of capital the organisation needs, and is responsible for safeguarding. For example, Forum for the Future identifies five broad areas of capital that organisations need to maintain.

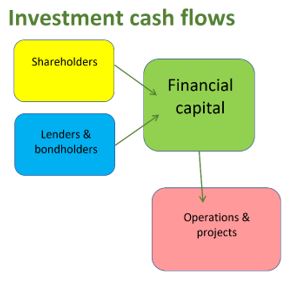

What shareholders do for our organisation

Focusing on financial capital and shareholders for now, a share in a company is a proportionate ownership right in the company. So the shareholders are the owners of the company. They invest money by buying shares, so providing financial capital to the company.

Financial capital also includes any money provided by lenders, usually for a fixed term. Capital is a source of finance for business operations, and also an investment for the capital provider.

Providers of financial capital generally require two things. (1) Information about their investments, to enable them to evaluate the level of risk they are exposed to. (2) Financial returns on their investments.

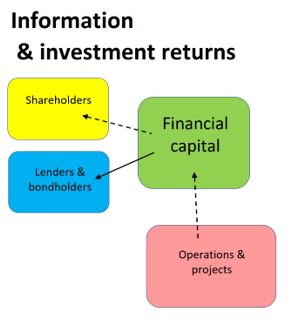

Notice the direction of the flows of information and investment returns in the diagram below. They are all in the opposite direction from the investment cash flows, above. Information and returns flow back, to the sources of the financial capital invested.

Investors make their investments in our capital in the expectation of a return flow of dividends or interest income and – in the case of lending – repayment of the capital amounts advanced.

Financial returns to lenders & shareholders

All investors want their invested capital kept safe. They also expect a surplus on top. This surplus is known as a return. It is often expressed as an annual percentage rate, to enable comparisons between different investments.

A rate of return on our activities is the financial surplus, expressed as a percentage of the capital invested in the activity or operation. Our cost of capital is the financial rate of return that our capital providers require on their investments. Our operating returns need to exceed our cost of capital.

If we can’t earn adequate rates of return from our operations to satisfy our capital providers, the capital providers will exit their investments if they can. This applies to all our stakeholders and areas of capital.

Interest & dividends

Interest is one form of return, generally calculated as a percentage of the amount deposited, loaned or borrowed. Interest is a type of investment income. Total investment returns include any capital gains or losses, as well as income. Interest and principal payments are contractual commitments of the company borrowing the money.

Dividends are amounts paid out to shareholders, from retained profits earned by the company, at the discretion of the company. The shareholders are the last to be paid. Looking at the diagram of investment returns above, notice the arrow back to our shareholders is dotted, emphasising the variable and discretionary nature of the dividends payable.

Stabilising operating surpluses

If there is nothing left over after paying everyone else, our shareholders get nothing. Shareholders generally need greater rates of return than lenders, to compensate the shareholders for the additional risk they undertake in being paid last.

The arrow back from our operations and projects to capital is also dotted, as a reminder that most operating profits and surpluses are variable, out of which we need to service all our capital providers - including fixed contractual commitments to lenders. Stabilising our operating surpluses will reduce the risk of shortfalls.

Stakeholders’ risks

For investors, key financial risks they are concerned about include (1) potential losses in the capital value of their invested money, and (2) potential reductions in the returns they expected when they made their investments.

Company directors and other senior managers have fiduciary and stewardship responsibilities for the assets they are managing on behalf of the owners, lenders and other stakeholders. This includes responsibilities for identifying, responding to, and reporting on the significant risks the organisation is exposed to.

Building well-founded confidence

Key dimensions of risk management include identifying – and prioritising – our organisation’s most significant risks. It also includes general organisational robustness and resilience, as well as specific sources of operational and financial risk.

Competent risk management and reporting will raise the market’s well-founded confidence in our organisation and its financial capital. This should reduce our cost of capital. The corporate function that communicates with existing and potential financial investors is known as investor relations.

Growing stakeholder value

Growth enhances corporate value, while mismanaged risk destroys it. Accordingly, managers can grow corporate value by appropriate sustainable growth of the future net positive cash flows of the business. In turn, this might flow from revenue growth, cost control – or both – assuming no change in related risk.

Similarly, all other things being equal, applying risk management techniques to reduce the risk of future cash flows will increase their value, via a reduction in the required rate of return for the (now) lower-risk cash flows.

In practice however, there will more often be a trade-off between improving – or worsening – forecast cash flows and related levels of risk. For example, discontinuing optional insurance cover will save insurance expenses, but increases the risk of uninsured losses. The sustainability of the entire business, including its environmental sustainability, has become an essential dimension of stakeholder risk management.

Working capital management

Working capital is the inventories and trade receivables, net of trade payables, that an organisation needs to carry out its operations. Working capital management is the appropriate management of working capital, to enable the continuation of operations in a cost-efficient way.

A subtle way to enhance shareholder value is to reduce working capital. One example is improving trade credit terms with customers and suppliers. In a simple case, this might enable the company to return capital to its shareholders for them to deploy elsewhere, while the company uses its remaining capital more efficiently, to continue to generate the same profits as before.

Measuring value – total shareholder return

One simple measure of shareholder value is share price. However, share price alone ignores any dividends enjoyed by the shareholders. Total shareholder return (TSR) factors in dividends and shareholders’ other relevant cash flows, as well as the capital value of shares.

TSR measures the internal rate of return (IRR) of all the cash flows enjoyed by an ordinary equity share investor. TSR takes account of the capital value of the shares over time, together with any dividends in the period, and any other cash flows between the company and its shareholders. Many listed companies use TSR as a key measure of senior management performance.

Many congratulations!

You have built a sound understanding of another important treasury concept.

___________________

Author: Doug Williamson, FCT